Markham & Associates, P.C.

Certified Public Accountant

Balancing the 199A Tax Credit to Your Indirect Cost Rate

Distribution Option:

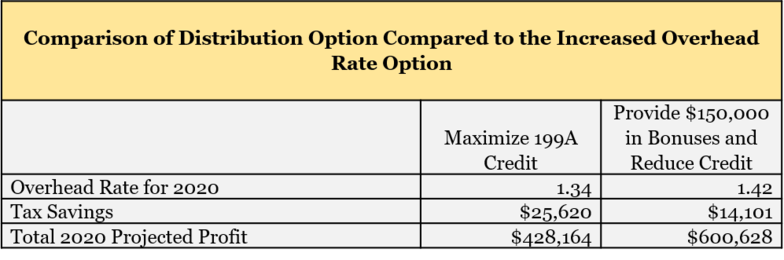

If Yellow Company were to take 100% of its profits as distributions the resulting 199A pass through deduction would be $86,407 ($432,036 x 20%). This would result in an estimated tax savings of $25,922 ($86,407 x 30% tax Rate) to the shareholders. The resulting 2019 overhead rate would be 134%.

If 2020 saw a 5% growth in direct labor ($1,995,000) and total expenses ($2,691,353) the revenue would be $5,114,518 and the net profit would be $428,164.

Increased Overhead Rate Option:

If Yellow Company were to move $150,000 into performance-based bonuses on a shareholder’s employee’s W-2 for 2018, then the company could take the remaining 199A deduction. The total profit would be $282,036 with a $56,407 tax deduction from 199A and a tax savings of $16,922. The resulting overhead rate to be used in 2020 would be 142%

Again, if 2020 saw a 5% growth in direct labor ($1,995,000) and total expenses ($2,691,353) the revenue would be $5,286,980 and the net profit would be $600,627. The increase in revenue is due to the 8% increase in the indirect rate x the total direct labor of $ 1,995,000.

As an S Corporation or other pass through entity, one is always looking to get the most out of tax saving strategies. One of the newest tax strategies is the use of the 199A credit. The 199A provision of the Tax Cuts and Jobs Act allows for 20% of profits of a qualified businesses to be tax-free income. In order to achieve the maximum credit many firms have reduced performance bonuses. This has resulted in a reduction of their current year expenses and can greatly impact the firm’s indirect cost rate. Which is better to take? Less bonuses to increase the tax credit or the maximum bonuses to increase the costs in the indirect rate with the potential to increase revenue in the future. Here, we consider a case study of what an engineering firm with governmental contracts should consider before closing their books for the year. It may be more prudent to pass on tax savings in the current year in order to increase revenue in the following year.

Which Is Better?

Tax Savings In The Current Year or

Higher Revenue In The Following Year?

It's A Balancing Act

In 1972, the Brooks Act (a US federal Law) established how architecture and engineering firms would be selected for design work on governmental contracts. Specifically, the governmental agency with the contract must select firms based on their qualifications, competency, and experience instead of the quoted price for the service. This is known as Qualifications Based Selection (QBS).

A large factor on the overall revenue of the company is the overhead rate that they are contracted under for these Government designs. The overhead rate is calculated based on the firms’ previous year’s financials through a “Statement of Direct Labor, Fringe Benefits, and General Overhead”. Another factor in a firm’s profits is how it structures its financials for tax purposes. Many engineering firms are setup as passthrough companies where they are not subject to double taxation. This includes the S Corporation and Limited Liability Companies (LLC).

The Tax Cuts and Jobs Act 199A provision allows for qualified businesses to take 20% of the profits as tax free. But, should an engineering firm take this tax credit? In many cases, the answer, maybe No. In fact, taking more bonuses and reducing the profits of the company could prove the sounder decision for these engineering firms. In the following case study, we will consider a hypothetical company’s decision to either take full advantage of the 199A provision or to increase their overhead rate for the following year.

What is the indirect cost rate?

Design firm’s reimbursement for a contract should be based on a fair and reasonable price. Part 31 of the Federal Acquisition Regulation (FAR) established to Over the years, the Government Agencies have worked toward interpreting the FAR and wrote the American Association of State Highway and Transportation Officials (AASHTO) Audit guide of 2016 that outlined the rules for determining allowable costs in the firm’s indirect rate.

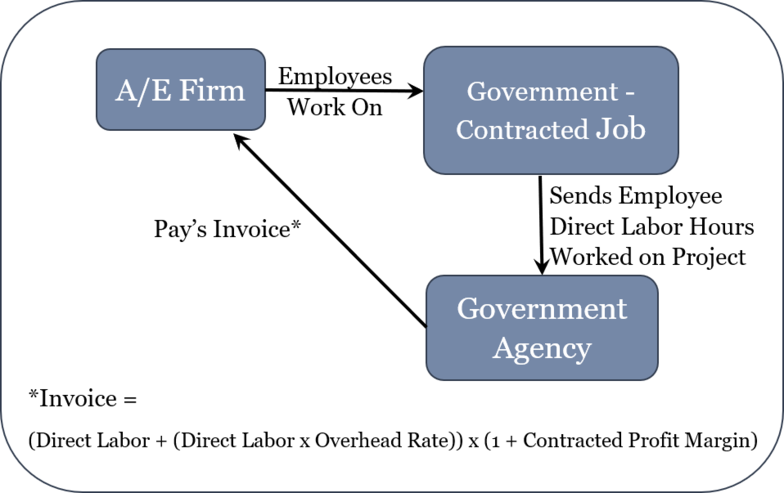

In many cases, Government Agencies uses an agreed upon “indirect cost rate” or “overhead rate” along with a contracted profit margin and direct labor to calculate a reasonable reimbursement rate. Figure 1 gives a high-level diagram of how a firm has employees work on projects then bills for direct labor to CDOT with a final equation used as direct labor cost plus direct labor multiplied by the overhead rate to give a total cost. Then the total cost is multiplied by one plus a profit margin of 7-15%.

Figure 1. High Level Invoicing Process For Engineering Firms and Governmental Agencies

Case Study

The Yellow Company:

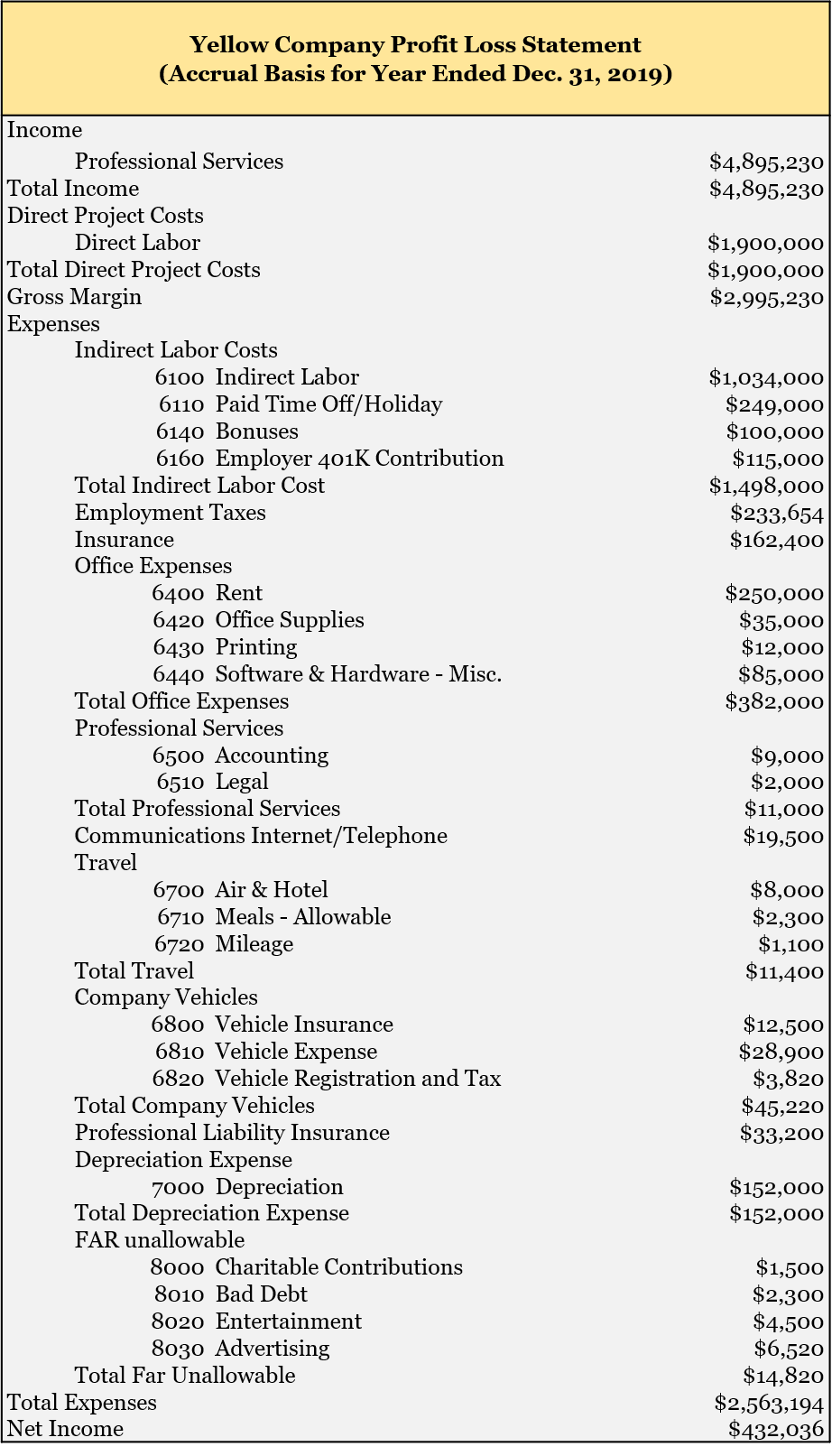

The Yellow Company is an engineering firm that provides construction inspection expertise to governmental entities. It is a S Corporation with three stockholder owners. One hundred percent of its revenue is from Government contracts with all revenue coming from reimbursement of direct labor combined with an overhead rate and profit margin. In 2019, Yellow Company had an overhead rate of 133% based on end of year 2018 financial data. It is now December 2019 and the accounting team is trying to decide if the company should distribute profits to stockholder equity or provide performance-based bonuses as additional W-2 compensation for the owners. The income statement for 2019 using the 100% distribution case is shown below.

Conclusion

So, based on this an engineering firm should always give bonuses instead of distributions? The answer is it depends on several factors and that an accountant that specializes in indirect cost rate planning could prove a great resource to consult on optimizing the overhead rate. There are rules on executive compensation and bonuses based on profit distribution that need to be considered with policies in the company set early to allow specific bonuses to be allowed.

Author: Daniel Markham, CPA

10/30/2019